CBSE Class 8 Maths Notes Chapter 8 Comparing Quantities Pdf free download is part of Class 8 Maths Notes for Quick Revision. Here we have given NCERT Class 8 Maths Notes Chapter 8 Comparing Quantities.

CBSE Class 8 Maths Notes Chapter 8 Comparing Quantities

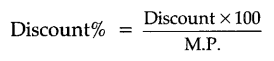

Discount is a reduction given on marked price.

Discount = Marked Price – Selling price.

Discount can be calculated when the discount percentage is given.

Discount = Discount % of marked Price.

Additional expenses made after buying an article are included in the cost price and are known as overhead expenses.

C.P = Buying Price + Overhead expenses

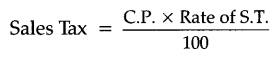

Sales tax is charged on the sale of an item by the government and is added to the bill amount.

Sales tax = Tax % of bill amount

VAT (value added tax) is charged on the selling price of an article.

Percent: The word percent is an abbreviation of the Latin phrase ‘per centum’ which means per hundred or hundredths.

M.P. = Marked Price

S.P. = Selling Price

M.P = S.E + Discount

Discount = M.P – S.P

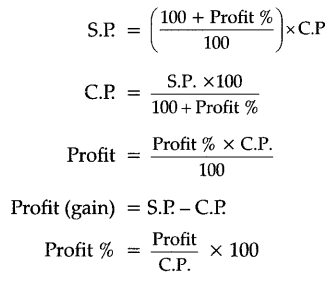

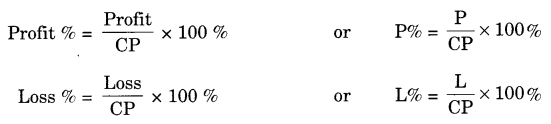

When profit % is given, then S.P > C.P and

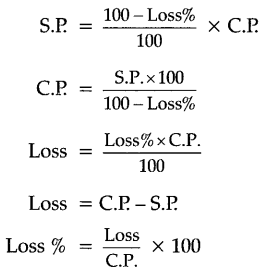

When loss % is given S.P < C.P and

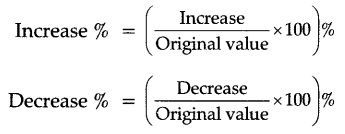

Increase and Decrease Percent

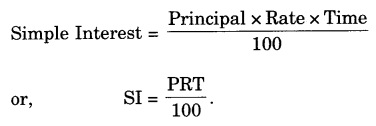

Simple Interest(SI): When the interest is paid to the lender regularly every year or half year on the same interest, we call it a simple interest. In other words, interest is said to simple, if it is calculated on the original principle throughout the loan period.

(S.I.=frac { Ptimes Rtimes T }{ 100 })

Where, P = Principal, R = Rate of Interest, T = Time.

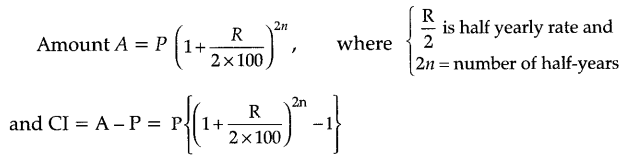

Compound Interest (CI): If the borrower and the lender agree to fix up a certain interval of time (say, a year or a half-year or a quarter of a year, etc.), so that the amount at the end of an interval becomes the principal for the next-interval, then the total interest over all the interval calculated in this way is called the compound interest.

Also, CI = Amount – Principal

(a) When interest is compounded annually, then

where P is Principal, R is the rate of interest and n is time period.

(b) When Interest is Compounded Half-Yearly, then

When R1, R2 and R3 are different rates for the first, second and third year, then

Recalling Ratios and Percentages

We usually compare two quantities by division, i.e., by using fractions.

Comparison by division is called ratio.

Note that two quantities can be compared only when they have the same units. Consequently, the ratio has no unit. However, if the two quantities are not in the same unit, then we convert them into the same unit before comparison.

Two quantities can also be compared using percentages. By percentage, we mean a fraction where the denominator is 100. The numerator of the fraction is called rate per cent.

For example: (frac { 5 }{ 100 }) means 5%. The symbol % is often used for the expression ‘per cent’ (p.c.).

To convert ratio into a percentage, we convert it into a fraction whose denominator is 100. [or we multiply by 100 and employ % sign.]

To convert percentage into a fraction, we divide the numerator by 100 and express it in the lowest form.

For example: 5% = (frac { 5 }{ 100 }) = (frac { 1 }{ 20 })

In unitary method, we find the value of one unit from the given value of some units and then we find the value of required number of units.

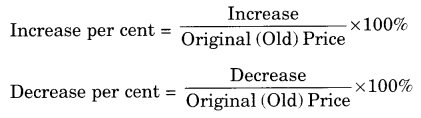

Finding the Increase or Decrease Percent

New Price = Original (Old) price + Increase

New Price = Original (Old) price – Reduction

Finding Discounts

Discount = Marked Price – Sale Price

Estimation in Percentages

- Round off the bill to the nearest tens.

- Find the amount of discount.

- Reduce the bill amount by discount amount.

Prices Related to Buying and Selling (Profit and Loss)

Overhead Charges

Sometimes when an article is bought, some additional expenses are made while buying or before selling it.

These expenses are sometimes referred to as overhead charges. These may include expenses like the amount spent on repairs, labour charges, transportation etc. These expenses have to be included in the cost price.

Finding Cost Price/Selling Price, Profit% / Loss%

Cost Price: The buying price of an item is known as its cost price. It is written in short as CP.

Selling Price: The price at which an item is sold is called its selling price. It is written in short as SP.

Profit: If SP > CP, then we make a profit.

Profit = SP – CP

Loss: If CP > SP, then we make a loss.

Loss = CP – SP

Note: If SP = CP, then we are in a no profit no loss situation.

Profit/Loss Percent:

Profit/Loss is always calculated on the CP.

Overall Gain:

Overall gain = Combined SP – Combined CP

Overall Loss:

Overall loss = Combined CP – Combined SP.

Note: We need to find the combined CP and SP to say whether there was an overall profit or loss.

Sales Tax/Value Added Tax

Sales tax is charged at a specified rate on the sale price of an item by the state government and is added to the bill amount. It is different for different items and also for different states.

Amount of Sales Tax = Tax% of the bill amount

These days, the prices include the tax known as Value Added Tax (VAT).

Compound Interest

Interest: Interest is the extra money paid by institutions like banks or post offices on money which is deposited (kept) with them. Interest is also paid by people when they borrow money. The money deposited or borrowed is called the principal. Interest is generally given in per cent for a period of one year.

Simple interest (SI): The interest is called simple when the principal does not change.

The formula for Simple Interest: Simple interest on a principal of ₹ P at R% rate of interest per year for T years is given by

Amount: Amount(A) = Principal (P) + Simple Interest (SI)

Deducing a Formula for Compound Interest

(A=Pleft( 1+frac { R }{ 100 } right) ^{ n })

where

P = Principal

R = Rate of interest per annum compounded annually

n = Number of years

A = Amount

CI = A – P

Rate Compounded Annually or Half Yearly (Semi-Annually)

The word annually mentioned after the rate means that the interest is charged at the end of every year, whereas the rate is given for one year.

We could also have interest rates compounded half-yearly or quarterly. This means that the rate for the one-half year (i.e., 6 months) is half of the rate given for one year and the time period is of two half years because interest is charged twice a year.

So if a sum of ₹ 50,000 is taken for 1 year at 10% p.a. compounded semi-annually, it means time period = 2 half years (i.e., 1 × 2) and rate = (frac { 1 }{ 2 }) × 10% = 5%.

Note:

- The time period for which the interest is calculated and added each time to form a new principle is called the conversion period or time period.

- If interest is compounded half-yearly, then there are two conversion periods in a year each after 6 months. In such situations, we compute the interest two times. So, the time period becomes twice and the rate becomes half of the annual rate.

- If interest is compounded quarterly, then there are four conversion periods in a year each after 3 months. In such situations, we compute the interest four times. So, the time period becomes four times and the rate becomes one-fourth of the annual rate.

Applications of Compound Interest Formula

We use the compound interest formula to find

- Increase (or decrease) in population.

- The growth of bacteria if the rate of growth is known.

- The value of an item, if its price increases or decreases in the intermediate years.

Note: For increase, R is positive and for decrease, R is negative.

We hope the given CBSE Class 8 Maths Notes Chapter 8 Comparing Quantities Pdf free download will help you. If you have any query regarding NCERT Class 8 Maths Notes Chapter 8 Comparing Quantities, drop a comment below and we will get back to you at the earliest.

<!–

–>